Attorneys representing a class of WWE shareholders argue based on their expert report that they are owed hundreds of millions of dollars, close to $1 billion by one formulation of their estimate. Another, seemingly even higher formulation, is redacted in the public version of the filed expert report.

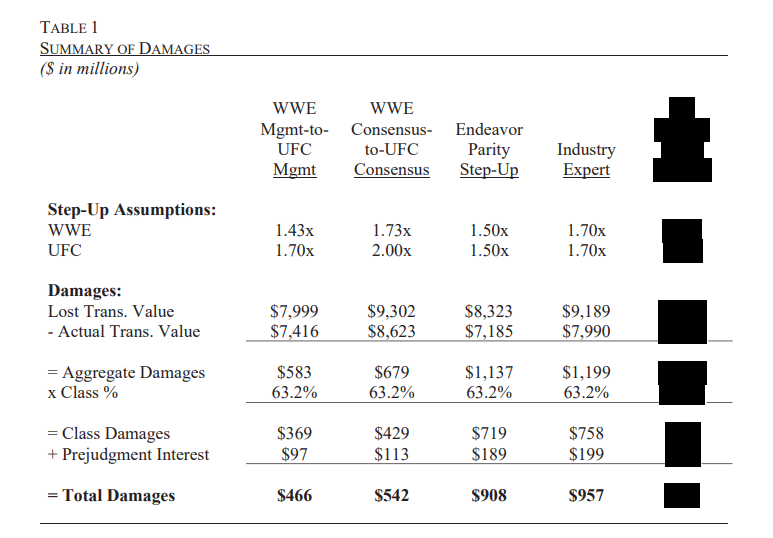

The monetary damages the plaintiffs are seeking range between $466 million and $957 million, plus interest. The range comes from an analysis written earlier this year by James L. Canessa, a financial economist retained by the plaintiffs.

The defendants in the case — who are Vince McMahon, Nick Khan, Paul Levesque, George Barrios, and Michelle Wilson — have retained their own experts who argue no damages at all are owed and that the deal that merged WWE with UFC to create TKO was fair.

The large sum of money the plaintiffs claim they are owed suggests the sides could be too far apart to come to an out-of-court settlement that would prevent the case from being litigated at a week-long trial in the Delaware Court of Chancery, scheduled to start next Monday, June 8.

If the plaintiffs win monetary damages, that money would be proportionally distributed to shareholders who held WWE stock during a relevant period to be determined.

The opposing sides’ experts are among those scheduled to testify at trial, in addition to an all-star lineup of WWE and TKO executives. Each of the defendants, as well as TKO CEO Ari Emanuel and President Mark Shapiro, is set to take the stand.

The plaintiffs allege McMahon unfairly steered the sale process in favor of Endeavor — which owned UFC — to secure his own future with the company despite allegations of sexual misconduct against him. The lawsuit claims McMahon’s preselection of Emanuel’s Endeavor prevented a fair and more competitive process from unfolding, which would have resulted in WWE selling for a higher price than it did. The defendants have denied the central allegations of the lawsuit.

A judgment in the case, determined by presiding judge Vice Chancellor J. Travis Laster, is expected some months after the trial concludes at the end of next week.

The case for the plaintiffs being owed nine figures in damages

When WWE and UFC merged, executives from WWE and Endeavor agreed in 2023 to an all-stock deal that resulted in Endeavor owning 51% of TKO and WWE shareholders getting the remaining 49%.

The deal was structured so that Endeavor, through its ownership of UFC, ended up with majority control and ownership of the combined company, which is the case today. The plaintiffs say that was wrong: WWE was worth enough that its shareholders should have come away owning the larger share, not Endeavor.

Their theory is that if you value WWE and UFC independently, WWE shareholders actually should’ve received the majority end of the deal: more like 53% to 57% of TKO, not the 49% that they got.

The difference between what WWE shareholders got and what the plaintiffs argue they should have gotten is what the lawsuit is trying to recover. The companies publicly valued the merger in 2023 at $21 billion. So a difference of just a few percentage points swings the math by hundreds of millions of dollars — or more.

The plaintiffs also point to a series of internal Endeavor presentations from the week before the deal was signed. A March 22, 2023, Endeavor document warned internally that “if we wait until after the media rights deal has been renegotiated, this merger will move away from us as the relative ownership will no longer be in our favor.”

In the plaintiffs’ view, this shows that Endeavor’s own executives put in writing that a fair deal would have given WWE shareholders majority ownership of TKO.

Note: This document has been filed publicly in In re World Wrestling Entertainment, Inc. Merger Litigation, despite earlier markings designating this material as confidential.

Why the plaintiffs say WWE was more valuable than UFC

At the time of the merger, not only was the company put up for sale, but it was also about to renew its valuable live broadcast rights for Raw and SmackDown, expiring in the fall of 2024. On top of that, UFC’s rights deal with ESPN would expire two years from the timing of the deal, in 2025. Both companies were expecting increases in their next deals. What’s being litigated now is how much was appropriate to expect.

In short, the plaintiffs argue that estimates for how WWE media rights renewals would go were too low and estimates for how UFC’s renewal would perform were too high, and that contributed to a misevaluation of the two companies.

Internal documents show WWE management projected a 1.43x increase (a 43% raise) in domestic rights fees for Raw and SmackDown. However, the plaintiffs’ media expert, Brendan Houlihan, argues WWE should have expected a 1.7x increase.

According to defense filings, Houlihan (whose report is not currently publicly available) arrived at the 1.7x figure by simply averaging WWE’s internal “low, base, and high-case” projections. The defense criticizes this, saying it ignores the fact that WWE executives explicitly designated the 1.43x figure as their most likely outcome.

As part of negotiating the deal, WWE’s management attempted to do its due diligence in understanding the value of UFC. The plaintiffs note that, according to then-WWE CFO Frank Riddick’s deposition testimony, Endeavor claimed it didn’t have forward-looking estimates to share with WWE.

Andrew Schleimer — then-UFC’s Chief Financial Officer and now TKO’s Chief Financial Officer — said at the time that such financial data for UFC didn’t exist. WWE was instead directed to base its dealmaking on outside analysis from Morgan Stanley that estimated UFC’s outlook and projected a 1.7x increase in UFC’s media rights.

But, the plaintiffs’ expert says, after the TKO deal was signed, in August 2023, Endeavor presented UFC projections that used a lower estimate of 1.5x.

The difference between a 70% increase in UFC’s media rights and an increase of 50% could be significant in evaluating the relative value of WWE and UFC. The plaintiffs use this as evidence to argue that WWE should have been assessed as more valuable than UFC, not less valuable.

The plaintiffs refer to internal communications at Endeavor in the days leading up to the UFC-WWE merger being signed, which emerged through evidence collection in this case, in which Endeavor executives say they have no UFC projections to share.

“In a March 26, 2023 email exchange among Endeavor and UFC personnel, Mr. Schleimer was informed that WWE’s financial advisors would ‘likely ask’ for UFC’s multi-year projections for purposes of their fairness opinions. Mr. Schleimer responded: ‘MS [Morgan Stanley] research.’ [Endeavor CFO Jason] Lublin complained: ‘How many time[s] are we going to say this[?]’ Mr. Schleimer further responded: ‘we won’t give projections or forecasts that do not exist.’”

In the plaintiffs’ framing, Schleimer admitted in his deposition stemming from this lawsuit that internal financial information on UFC did, in fact, exist.

“At his deposition, Mr. Schleimer conceded that such projections did exist and that ‘UFC forecasts were not provided’ to WWE. Mr. Schleimer initially sought to justify the failure to provide projections to WWE by testifying that, ‘for purposes of this deal, we were focused on Morgan Stanley research for UFC… Mr. Schleimer testified that his assertion that projections ‘do not exist’ was ‘[l]ikely positioning from my own team.’”

How WWE and UFC media rights renewals actually performed after the merger

In reality, UFC’s new deal with Paramount for $1.1 billion per year represented an increase of about 2x in rights fees from the previous deals with ESPN — significantly outperforming either of the 1.5x or 1.7x estimates.

And in reality, for WWE, the increases — through new deals with Netflix for Raw and USA Network for SmackDown — were more modest. It’s difficult to unpack the exact rate of increase for the Netflix deal because the streamer got not only domestic rights to Raw but also the majority of WWE’s international rights. However, the SmackDown deal was an increase from $205 million per year with Fox to $287 million on USA, a step-up of 1.4x — a raise right in line with WWE’s internal estimates.

The defendants’ expert rebuttal report notes that WWE management actually used step-up assumptions very close to those actual results: 1.43x for WWE and 2.0x for UFC.

Professor David C. Smith is retained by the defense. He points out that Canessa never ran a damages scenario combining those two assumptions together. When Smith does so using Canessa’s own methodology, Smith finds that the calculated damages fall to zero.

Note: This document has been filed publicly in In re World Wrestling Entertainment, Inc. Merger Litigation, despite earlier markings designating this material as confidential.

Defendants’ experts push back

Smith argues in a written rebuttal that the synergies WWE and UFC enjoy by being combined aren’t properly accounted for in the plaintiffs’ expert report by Canessa.

Synergies here refer largely to cost savings: staff lay-offs, as well as revenue opportunities that could be unlocked by selling WWE and UFC together. Smith writes that accounting for synergies, the fair split for WWE may have been as low as 48.1%, slightly lower than the 49% shareholders got, arguing that investors actually got a more-than-fair deal.

The defendants have retained three experts for the case: Smith, Professor Steven Salaga, and Doug Perlman. The plaintiffs have two experts: Canessa and Houlihan. At the time of this writing, only materials from Canessa, Smith, and Perlman are publicly filed.

Smith is a business school professor at the University of Virginia McIntire School of Commerce. Salaga is a professor and program coordinator for the Sport Management & Policy program at the University of Georgia. Perlman is the CEO and founder of Sports Media Advisors, LLC. Canessa is the President of consulting firm CE Financial Economics, Inc.; he specializes in providing expert witness testimony. Houlihan is a Managing Director at Salem Partners, with more than 20 years of experience advising on M&A transactions.

TKO stock price growth may not be relevant

When the TKO deal closed in September 2023, WWE shares immediately converted one-for-one to TKO shares. Since that time, those shares have roughly doubled in value, well above the performance of indexes like the S&P 500. However, that growth may not be a major issue in this case. The plaintiffs’ broader allegation is that the process McMahon ran was designed to favor Endeavor, which kept WWE from being properly valued in 2023.

The plaintiffs’ theory for monetary damages doesn’t require proving that WWE should have sold to a different buyer. Even in the scenario where a merger with UFC still happens, the plaintiffs argue the ownership split should’ve given WWE shareholders the majority stake, not the minority one. And, separately, they allege that other bidders like Formula One parent Liberty Media and private equity firm KKR weren’t given a fair chance to compete, which the plaintiffs say would have driven up the price regardless of who ultimately won.